Bankruptcy with Chinese Characteristics

What is the nature of local government debt in China and what does it reveal about the true state of the country’s financial system?

“China prepares to resolve outstanding local government debt”, “China's local government debt remains low”, “Local govt debt 'uneven' but tolerable”.

These are all headlines from China’s national newspaper China Daily from the first half of this year. According to the CCP, not only is local government debt in China completely manageable, the nation’s “overall fiscal condition is seen as healthy, sound, with ample scope.” According to internal figures, China's statutory debt-to-GDP ratio came in at around 50 percent last year “relatively low by global standards and below the international warning line of 60 percent”.

And yet, despite the optimism from the Chinese side, external headlines seem somewhat contradictory in tone, with recent titles such as: “China’s cities are on the verge of a debt crisis”, “China's $23 Trillion Local Debt Mess Is About to Get Worse” “China’s local-debt crisis is about to get nasty”.

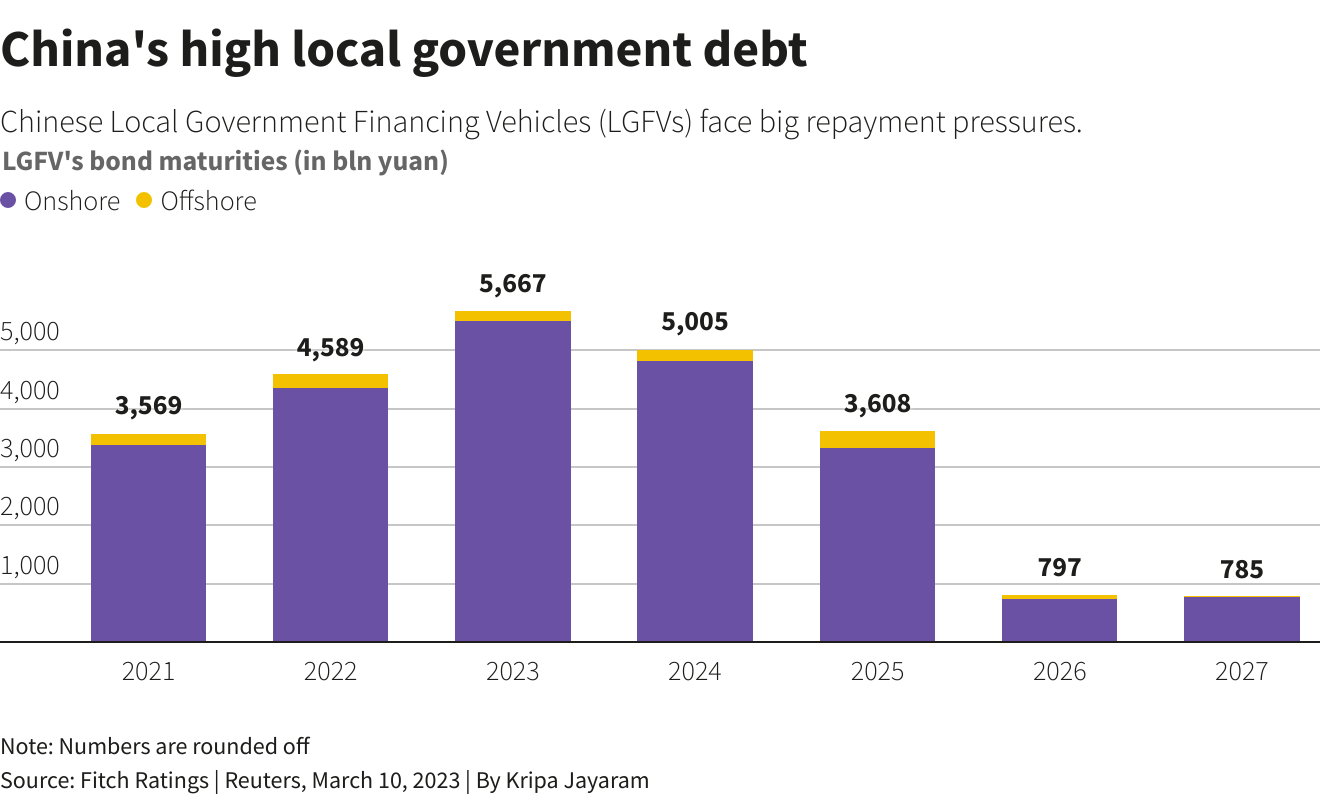

It’s not as if China is unaware of the problem of local government debt, nor are they necessarily trying to hide it. However, the government and party seem very confident in their ability to keep the situation under their control. The CCP in January made it clear that it would be resolving hidden local government debt without bail-outs from the central government, instead seeking out “law-based” and “market-oriented” ways to defuse risks and introduce regulation to oversee local government financing vehicles (LGFVs), state-owned companies set up to finance local government investment such as building infrastructure.

China is keen to highlight the fact that not all government debt is bad debt. When used correctly, government debt can boost growth and finance important infrastructure projects that provide the foundation for local economic development. Just this year for example local governments have issued around 4.4 trillion yuan of bonds, partly to repay the principal on outstanding debts, and partly to pay for new infrastructure projects such as the building of industrial parks, transportation, social business, affordable housing projects, and other major projects in significant sectors such as agriculture, forestry, water conservation, and ecological and environmental protection.

China also tends to rest heavily on macroeconomic trends that often play in their favour:

China's economy continued to recover in the first quarter, and market confidence and expectations improved significantly, according to the Bank of China Research Institute… Data from the General Administration of Customs last week showed that foreign trade has been improving over the past three months. As for the financial sector, the growth of yuan-denominated loans amounted to 10.6 trillion yuan during the first quarter of this year, up 2.27 trillion yuan from a year ago, "The yuan loans growth hit a record high in the first quarter of this year as sustained economic improvement led to a rebound in corporate loan demand," said Wen Bin, the chief economist of China Minsheng Bank.

But these macroeconomic figures are disguising a huge problem lurking just beneath the surface. At a local level, governments are struggling to stay afloat as infrastructure projects fail to provide ROI, land sales continue to flounder, and hidden debt mounts. While there are no official figures on the total debt of local governments (I doubt the CCP would ever release that information), China has admitted that it is at least USD$3 trillion. How did they get into this much trouble? The answer lies in how local governments make their money in the first place.

The problem

Chinese municipalities are given certain budgets and technically were not allowed to overspend or run deficits, or even borrow externally until 2014. A workaround that was developed was the creation of LGFVs, a state-owned enterprise (SOE) with the corresponding government as the only or major shareholder, through which it can borrow money via bank loans. The majority of these LGFV loans are issued as bonds that go towards financing urban development, everything from small building projects to the development of entire industrial parks with facilities and offices ready for use. The use of LGFVs was heavily encouraged by the central government following the 2008 financial crisis and Sichuan earthquake when economic stimulation and infrastructure development was desperately needed.

But after 2014, the central government ordered LGFVs to detach themselves from local governments and become normal, independent companies that are no longer just for government use, but can function as the ‘private sector’ in public-private partnerships. This put LGFVs in an awkward situation, where they’re not quite SOEs and not quite private companies. They still have the clout of being guaranteed by the local government, but can now operate like a proper financial company that abides by market rules. Now they basically perform the same role of acting as an intermediary for bank loans (most articles treat LGFVs and government debt as the same thing) but without the guarantee of the government backing up the loan.

Why have I taken so much time to outline all this complicated waffle? Because within this waffle lies the key to understanding the circular nature of debt in China’s municipalities.

Local governments borrow money from LGFVs, usually backing up their loans with physical assets like land. The LGFVs then use this land to back up their own loans from banks, expecting to sell this land on to developers who will make new houses, which will be sold to customers, pay the LGFVs, who will then pay back the banks, and then everyone is happy. But this plan fell to pieces when China’s housing market began to crumble. I’ve made an entire podcast episode on this so I won’t go over it again in detail here, but essentially China’s property developers have been struggling to finish properties on time, or have been doing so to poor standards. This has led to a fall in confidence in buyers, which has left many overleveraged developers on the edge of default. While there has been some recovery in the property market, in 2022, land sales fell 50%. With no home sales, property developers can no longer afford to buy land. How important is the sale of land to local governments?

According to Yicai Global's calculations, land transaction payments have accounted for over 30 percent of total local government fiscal revenue for five straight years since 2017, and the ratio was over 40 percent in 2020 and 2021.

You probably don’t need to know this much detail, but what I want to drive home with all of this is the fact that because of the way that local governments borrow money and use LGFVs, a lot of debt that technically belongs to them is not being attributed to them because it’s ‘hidden’. Hidden debt is what the central government terms “liabilities beyond the legally mandated government debt limit.” Local governments hide money in public-private partnerships, again, usually through deals with LGVFs. The amount of hidden debt held by local governments ranges: while internal figures from the National Audit Office pointed out that 49 regions had CNY41.5 billion (USD6.2 billion) of illegal new hidden debt, external analysts from places like the IMF put the number between 30 trillion yuan and 70 trillion yuan.

If any local government or LGFV defaults on a loan the effects on the country’s financial and economic system could be potentially devastating. The beginning of this process is already starting to rear its head.

The manifestation

One of the things the Chinese government is able to admit is that “the main problem facing China's debt issue is that debts are distributed unevenly across regions, with some regions facing higher debt risks as well as pressure in paying interests and principles.”

If we look at the spread of debt across China’s regions, historically poor regions like Guizhou are suffering the worst:

The province is said to owe about 2.6trn yuan ($380bn, or 130% of local gdp) in various forms including bonds and opaque debts owed by local-government-financing vehicles (lgfvs)... Interest payments make up more than 8% of the province’s fiscal expenditure, compared with a national average of 6%. Some cities in the province are already spending most of their funds merely to pay off debt. In Guiyang annual interest payments equal 56% of yearly revenues.

There is little hope of bringing in more revenue to meet the costs. The area has always been an economic backwater: the local topography is one of endless misty hills that for millennia made travel hard and villages poor. Guizhou’s economy is reliant on the connectivity brought by its new roads and tunnels. Many locals are farmers. The region does not have much manufacturing, and has just one important corporation of which to speak: Moutai.

The region’s lgfvs have already experienced more than 20 defaults on trust loans and other hidden debts since the start of 2022, many more than in other provinces.

Clearly, Guizhou’s government thought that debt financing would lead to rapid development and a reversal of fortunes. But debt as a vehicle for growth only works if government debt levels remain reasonable and local governments don’t get too ahead of themselves, expanding their cities too quickly and not being able to meet expectations down the road. Another good example of this is Tianjin.

“Tianjin, like other parts of China, has relied on government-owned companies to pay for investments. Zhang Zhiwei, an economist with Deutsche Bank, has estimated that in Tianjin these companies only have enough revenue to cover about 40% of what they owe in interest, the third-worst ratio among China’s provinces. Tianjin is, he says, a “pilot experiment” for how the government will resolve its debts.

The experiment is not going all that well. In May two city-owned developers flirted with defaults on loans that together were worth 700m yuan ($103m). In both cases they conveniently came up with cash in the end. But some analysts saw that as a missed opportunity. In the absence of genuine defaults banks will go on lending to rotten state firms, knowing the government will always prop them up.”

The Bailout

The most frustrating thing about this situation is probably that we will never know the true scale of the problem because the central government will not allow the localities to fail.

After saying they wouldn't bail out failing property developers, the central government is the only thing keeping the industry afloat. The truth is that apart from the unlucky ‘home’ owners, the hardest hit by a potential collapse of China’s housing industry would be local governments, who will lose out not just on much needed revenue sources, but also the potential to expand urban areas. If a new city can’t provide housing, and instead is littered with abandoned lots and half-built towering shells, it’s only a matter of time before it slides off the map, no matter how shiny and new its infrastructure is. It will be interesting to see how this situation is exacerbated by declining population levels in the next half of the century too.

The central government has also said that it won’t bail out LGFVs or local governments in bad debt. “If it’s your baby, you own it.” said Finance Minister Liu Kun. But the central government is intently coming up with more and more schemes to get local governments out of trouble, from setting up "swap bonds," where debt is exchanged for local government bonds to bring off-balance-sheet borrowings onto their books, to literally sending cash so that governments don’t default. While it’s billed as helping out local officials, the truth is there’s no way to bail out a province without bailing out the corresponding LGFV:

The central government is transferring funds to localities on a grander scale than ever before. More than 30trn yuan was made available between 2020 and 2022. An lgfv in the city of Zunyi, in the indebted south-western province of Guizhou, recently agreed with local banks to lower rates, defer principal payments for ten years and extend the maturity of its debt to 20 years. Such arrangements could become more common in future. Proponents argue they indicate a genuine willingness on the part of local officials to pay their debts, and are an acknowledgment that it will simply take more time than expected.

But ever-growing debt over the past decade suggests that many projects will never become truly profitable, says Jack Yuan of Moody’s, a ratings agency. The troubled lgfv in Zunyi, for instance, has had negative cashflows since 2016, and seems to have little hope of a turnaround. - China’s cities are on the verge of a debt crisis, The Economist

The CCP cannot afford to let local or provincial governments fail, as that would not only undermine their own plans for urbanisation and the dual circulation economy, but it would also make China an unattractive prospect for foreign investors. The central government will continue to put out fires and rescue failing investments for as long as it can, but whether or not they will ever be paid back is a different question: “if these governments could not make payments when local gdp growth was high, often above 7%, how will they manage in the forthcoming decade, with growth of perhaps 3%?”

But that’s a future problem. The main task of the central government now is to solve the fundamental issues plaguing local economies before time runs out. In the meantime, they’ll have to remain poker faced and keep pretending that everything is OK, while praying for a miracle windfall before provinces collapse like dominoes.

Sinobabble Extended Universe

The latest podcast episode is about Socialism with Chinese Characteristics. Listen here, on Spotify, Apple Podcasts, Google Podcasts, or on Youtube.

Support my efforts! Buy me a coffee 😊